Not being a tax expert, nor being personally affected, I can’t stay how this would impact on members of this forum, but it looks as if those Chileans and Residents who receive income from abroad now are expected to voluntarily declare, and pay a tax on it, even if it has been declared in the country of origin.

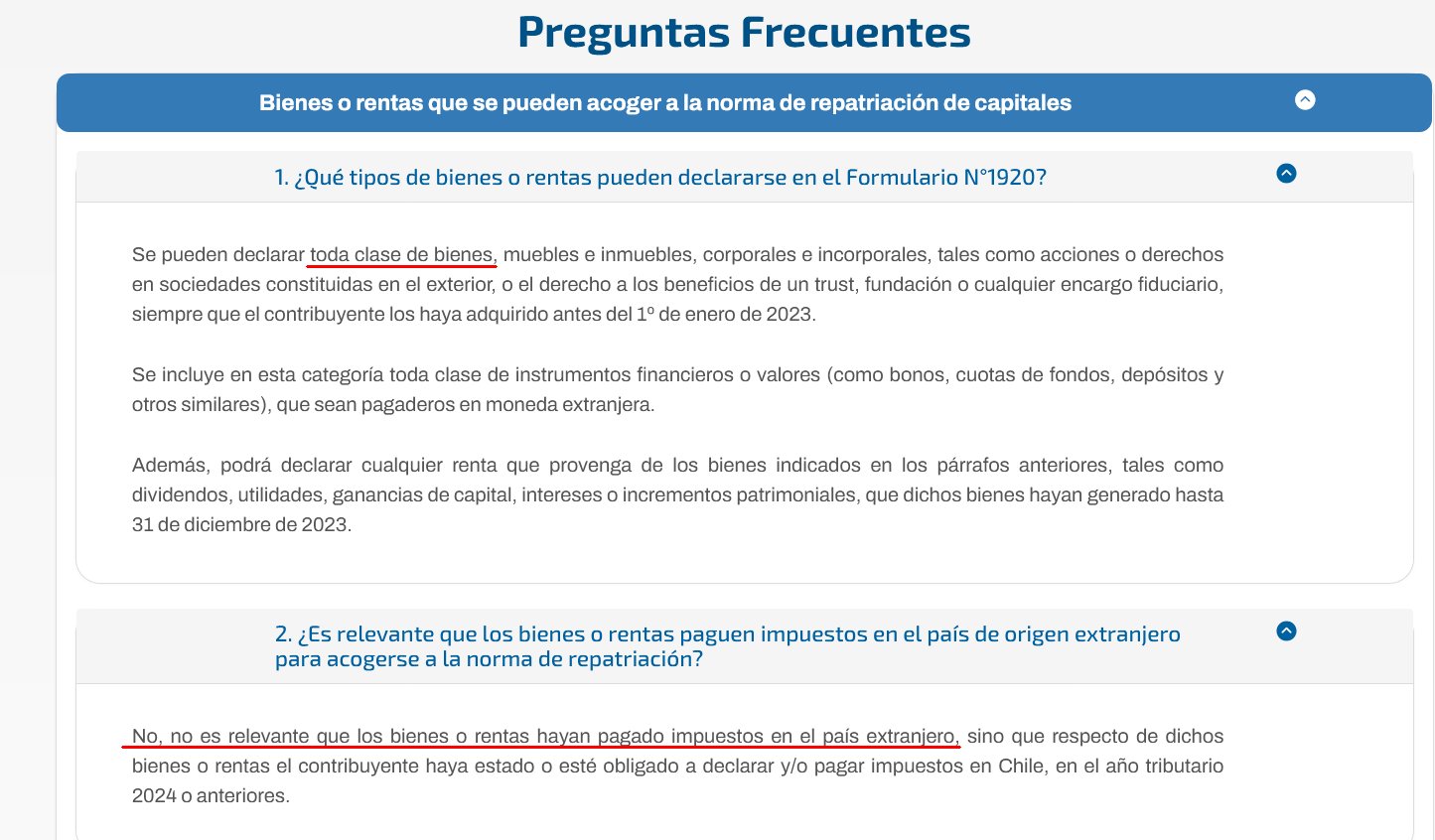

En detalle, esta repatriación de capitales consiste en un impuesto único y sustitutivo, con una tasa de 12%, sobre el valor de los bienes o rentas determinado por el contribuyente.

By the way, for non-Spanish speakers, I did a google for “new tax rule 1920 chile” and there were a bunch of websites talking about it.

When it says “declaración de bienes o rentas que se encuentren en el extranjero” “rentas” could mean salary - or similar ongoing earnings from work. However it later says “renta que provenga de los bienes” which refers to earnings from assets and investments and would exclude salary or similar.

I pay my taxes on earnings using F22 form once a year in about April or May. I’ll perhaps do the same and ignore this?

Basically, if you have ANY assets or income or jobs or accounts or companies or trusts or retirment accounts or stocks or bonds or real estate or rental income…yes anything…outside of chile or in the past have had assets or beneficial interest in any of the above outside of chile…well you have until Dec 31 2024 to report everything that hasnt been disclosed to chile previously and possibly pay a 12% tax on what chile lays tax claim on…even if it no longer exists due to being spent or liquidated or sold, etc.

Our considered opinion is that such a statement is not entirely correct.

Don’t some countries have tax treaties with Chile to prevent what is essentially double taxation of such income? And does the Chilean law exclude retirement pensions paid by other countries?

To wit, SII has a page, updated in 2023, que reza:

Las pensiones de fuente extranjera recibidas por una persona que tiene domicilio o residencia en Chile, ya sea chileno o extranjero, son ingresos que no se consideran como renta. Por esta razón, dichos ingresos no están afectos a impuesto, según lo dispuesto en el Artículo 17, N° 17 de la Ley sobre Impuesto a la Renta.

(Unofficial translation: Foreign-sourced pensions received by persons domiciled or resident in Chile, whether Chilean or foreign, are not considered as income. For this reason, such monies are not subject to tax, according to the provisions of Article 17, No. 17 of the Income Tax Law).

This retirement exemption message is consistent with the opinion of the local [Punta Arenas] SII office people, and would contradict the opinion previously expressed by “mem.”.

This subject matter is or can be enormously complex and with continuing changes, so dynamic that it is hard to keep pace. I noticed that SII has an English language page with the following.

On that page the term FCT is used as the abbreviation for what they call First Category Tax, which we all know is really the more familiar “Impuesto de Primer Categoría” which is normally a “business tax.”

The date on that SII site entry is year 2000 so much of that material may be out of date but some of the concepts likely still apply :

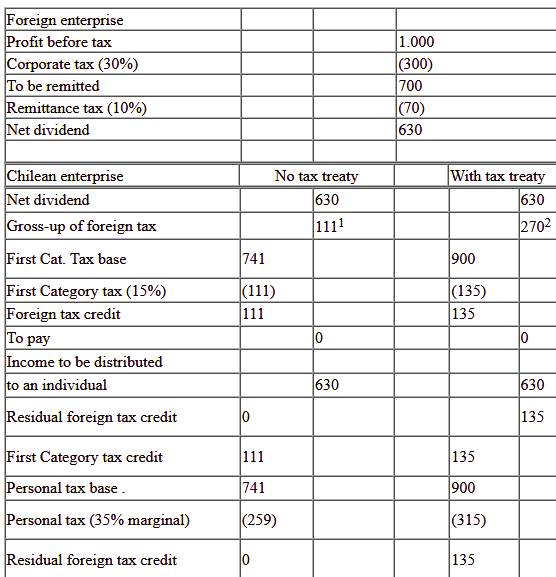

VI. FOREIGN TAX CREDIT

Foreign taxes may be credited against domestic taxes or treated as a deductible cost. Unilateral tax credits up to 15% are allowed on some foreign source income. With a tax treaty a credit of up to 30% is allowed. Excess credits may be carried forward.

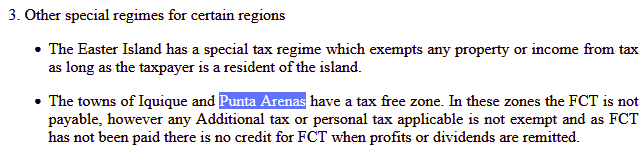

In the following, where the SII page says " towns" this may be misleading and possibly the exemption applies to the entire Zona(s) Franca de Extensión but that needs to be clarified. There may be others among our number who live in the exempted Zonas Franca de Extensión (regions - extreme north and south)

An unreliable local club member (read: “shithouse lawyer”) offered a dubious observation about foreigners who do not meet the standard for Chilean legal resident (which was Tompkins case – he was a famous tax-evader in Chile, by retaining “tourist” status and never becoming legal resident under the then-prevailing rules – an observation made by congressional people here who were critical of Tompkins’ activities). This opinion I refer to was that such nonresident foreigners can live in Chile for up to six years without being obligated to pay taxes on foreign (non-Chilean income). That would need to be investigated and confirmed.

With respect to the apparently perceived need to make an annual declaration of income, SII has indicated that this is only needed if your income, in the case of only Chilean sources, exceeds CLP 10,402,992 (for 2024).

En fin, this entire subject is something to be referenced according to the specific provisions of prevailing law.

Of course it would be too much to expect the SII to decently explain their intentions here, especially when there are specific provisions in the tax code to avoid Double Taxation.

As for the “voluntary” aspect of this declaration, who is going to voluntarily declare income unless omission is a punishable offense?

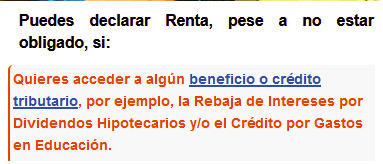

There are actually situations where voluntary income declaration provides benefits, or rather provides the basis for receiving certain benefits, such as credits for educational expenditures, credit for payments of “contribuciones” and so on. That includes opportunities for refunds of withholding (“retenciones”). The actual mechanisms and details for taking advantage of these benefits are more complex than I want to try to explain here, but it should suffice to say that a truly competent tax accountant should be consulted by anyone interested in taking advantage of these credits. Some of this is briefly illustrated on the SII web pages.

If your foriegn pension or retirememt is paid to you in a foreign bank account…has that bank account been declared to SII?

That is the issue. The complete disclosure of ALL foriegn accounts and assets and not just what the balances currently are…but what they were.

If your foriegn pension or retirment is paid into a chilean account then sure no problem.

This is what this amnesty program is about. The part where they ask question about the makeup of those balances come later…once you have made a complete declaration with nothing left out

Oh yes…omission absolutely is a punishable offense.

In fact the entire purpose of this amnesty program is a tradeoff. You voluntarily disclose all foreign accounts and assets and income streams by end of Dec 2024 and you will not be criminaly prosecuted for not disclosing them sooner and you only have to pay 12% tax on the amounts that SII deems taxable.

Part of the key to understanding this issue is found in this part:

…respecto de bienes y rentas que se encuentren en el extranjero, cuando habiendo estado afectos a impuestos en Chile, no hayan sido oportunamente declarados…

If income is not “afecto a impuestos en Chile” then is it understood that there is no obligation to make a declaration, or to include non-affected income streams in declarations. As always, what income may be subject to such taxation is the territory of someone with the appropriate knowledge of the entire range of the relevant tax law. Slds.

Again this is about things like bank accounts or assets where various forms of income are stored. Sure as long as all the foriegn bank accounts and assets and the present and historical balances are declared to chile that is what matters to Chile.

If you had a foreign bank account that had only 100% retirement/pension funds ever, from inception, and also never bore a cent of interest on the balance…sure you could roll the dice and not disclose it. But if Chile finds that undeclared bank account via a tax treaty information exchange then they will assume there is a problem, and the burden of proof will be on the account owner to prove no other funds were intermingled there and that the account has and has always had a 0.00% interest rate on it

Just look at this administration. Believe them when they say they are looking to find every cent for the coffers. Take no chances.

I issue boletas monthly with a RUT to be used for international clients who don’t have a RUT (44444446-0). I’m doing work for a company in the US. I then declare Form 29 monthly and pay the retention. At tax time, I declare Form 22. So, I should be covered there.

The only other assets I have in the US is a 401(k) rollover. When there was first talk of this, I asked my husband and he said I wouldn’t need to declare this. He’s a lawyer and has taken various tax law classes. I think I will have him take a look and confirm that this is the case. That would really suck if I had to pay. It’s not a small amount.

My opinion is it sounds like your 401k should not have any non-401k funds intermingled. I dont think it would be taxable at this point presuming you are not taking anything out of it.

With social security payments that are made from the US government to a retirees regular US bank account…that generates interest and likely has other monies coming and going from that account…that account would be one that chile would want reported.

Likewise if you opened an interest bearing checking account in the US when you retired and started taking distributions from your 401k with the distributions going into your interest bearing US checking account. That US checking account would be reportable. If the checking account doesnt have interest generated and you dont intermingle any other non-401k monies in that checking account then it wouldnt be. Again my opinion of what I have read.

Keep in mind reporting something doesnt necessarily mean it will be taxed in whole or in part, but it certainly could be depending on the perspective of Chile. It is just a way to cover your bases against criminal charges by Chile if they find something that wasnt disclosed and there is a difference of opinion on whether it should have been disclosed or not.

Pretty much this is like Chile’s version of FATCA with an eye to goosing the coffers for the administrstion. Keep that in mind and act accordingly

FYI, this power grab is part of the SAME BILL that eliminates the $41 dollar mail order import exemption, institutes the 50 or 100 electronic transfers flag, permanently brings taxation to the social media sphere and probably will be the reason why we may soon need to show a cedula for cash deposits with perhaps having to give a for the record reason for them and their origin. Did the a$$e$ in Congre$$ realize that this will also affect them along with a large part of the mostly law abiding population and not just the hated “big business”, “suit and tie” criminal and organized crime sectors? And attracting rich expats will definitely be out of the question and losing them perhaps a near done deal.

And why the tight time frame for voluntary “reporting”? Why no MSM coverage over this aspect of the new tax law that is sure to affect a large number in the upper middle to above classes? It’s like the intention is to turn a large number into technical tax violators to increase fines and impose more control.

To make it political, I heard it was only the Republicans who voted against this tax bill.

Wait and see, and I hope someone with expertise will post.

Another aside, this hard handedness coincides with my experience back on Oct 25 when the Aduanas guy at SCL lectured me on my supplements, asked the value of the powerbanks I was bringing in as gifts and even about my finances (haven’t had such questions since 2002 when on my first trip back to the Statesaka as the US or the Empire after 9 1 1). My news research showed this the day the Boric admin celebrated with officials among them Aduanas on the new tax law.

Dummy me. A whole day researching shit to feel like shit.